Define an 'emerging' market

When constructing portfolios, index selection is often treated as a secondary consideration - something that sits behind higher level decisions like asset allocation or risk tolerance. In reality, the choice of index provider can introduce meaningful differences to both exposures and outcomes, even when two funds appear to be targeting the same part of the market.

A timely example of this in 2026 is South Korea. The market has been one of the standout performers year to date, delivering returns of roughly +44% in GBP terms. However, investors may not realise that their exposure to Korea is not simply a function of their asset allocation - it is also determined by how their chosen index provider classifies the country.

FTSE classifies South Korea as a developed market, meaning it is included within developed world indices. MSCI, on the other hand, continues to classify Korea as emerging. For investors combining developed and emerging market funds, this creates a subtle but important challenge. Depending on the combination of indices used, Korea can be entirely excluded from a portfolio or, conversely, double counted.

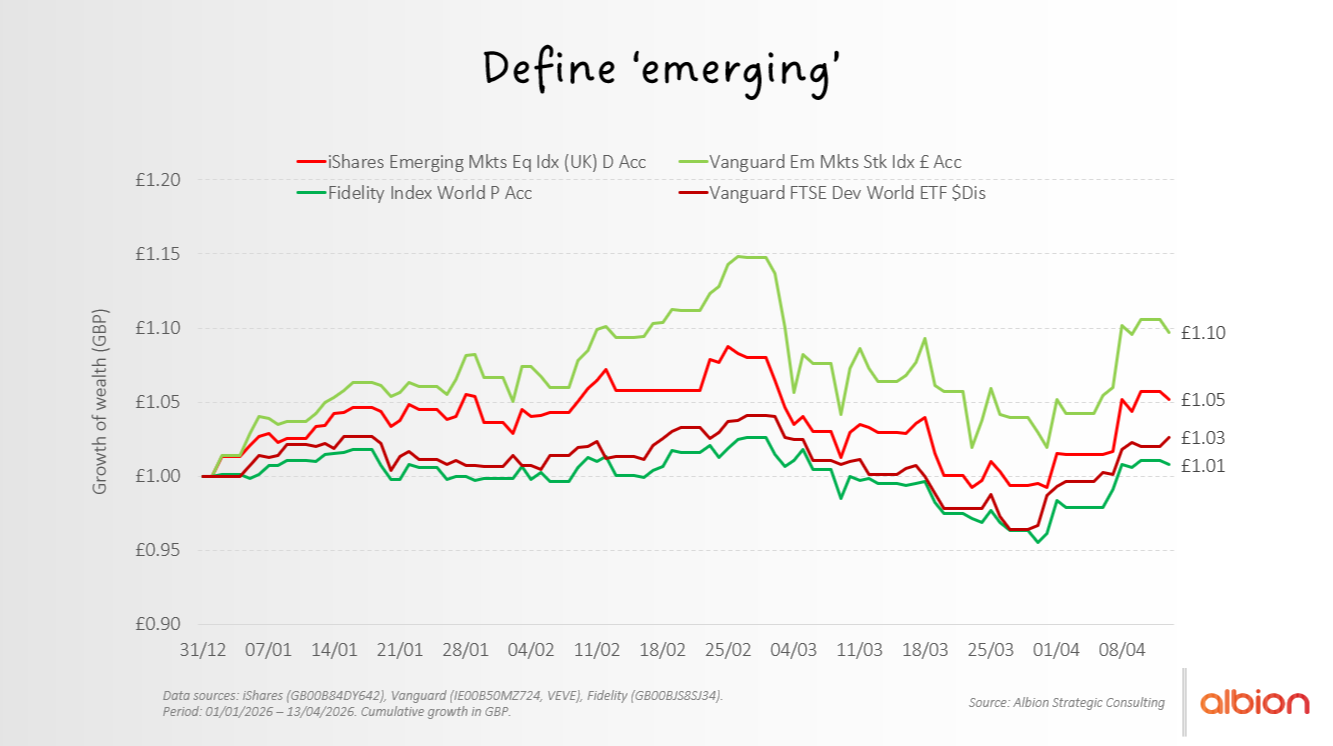

YTD 2026 performance highlighting the impact of South Korea’s classification differences across FTSE and MSCI index frameworks.

The chart above illustrates how this has played out in practice so far this year. Portfolios using FTSE for developed markets and MSCI for emerging markets have benefitted from an overweight exposure to Korea, while those using the reverse combination have missed the rally entirely. Despite representing only around 2% of global market capitalisation, the strength of returns has meant that these differences have had a noticeable impact on overall performance.

While South Korea provides a clear and timely case study, it is just one example of a broader point. Index providers differ across a range of dimensions - including security selection, weighting methodologies, rebalancing approaches and the treatment of corporate actions. These differences, while often viewed as technical details, can compound over time to create meaningful variation in outcomes.

The purpose of this piece is not to suggest that one provider is inherently superior, but rather to highlight the importance of understanding what sits beneath the surface. These structural nuances are frequently overlooked, yet they can matter far more than marginal differences in cost. As ever, this content is provided for educational purposes only and should not be considered investment advice.

Related Blogs

Diversification vs Duplication

Many portfolios that appear diversified are actually concentrated in the same stocks — leading to duplication, not true diversification.

Read more

The emotions of investing

Humans aren't wired to be good investors

Read more

The Voting Machine vs. The Weighing Machine

Don’t get lost in the noise.

Read moreGet in touch

Don't hesitate to get in touch - we would be delighted to receive your call or email. For enquiries about our service, please use the contact form and one of the team will respond in due course.